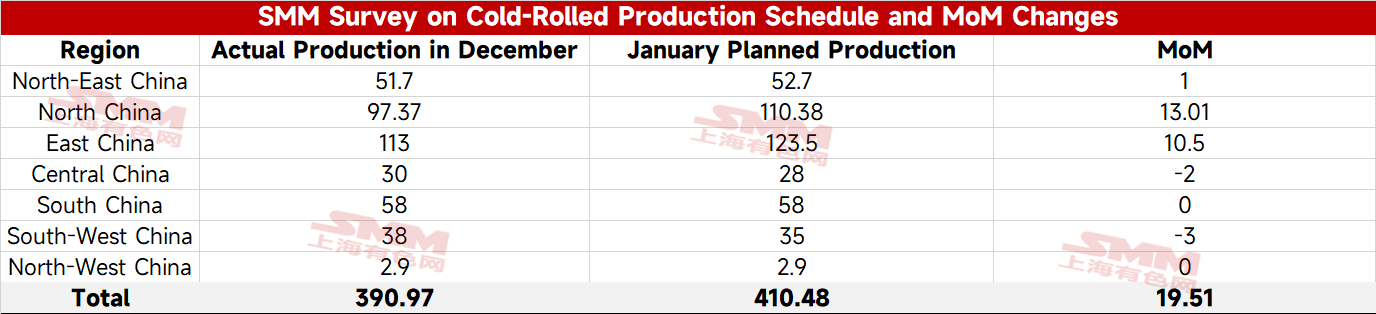

- SMM Cold Rolling Production Schedule: Cold rolling production schedules at steel mills increased by 5% MoM in January.

According to the latest SMM tracking, the total planned volume of cold-rolled commercial steel from 31 mainstream steel mills was 4.1048 million mt this month, an increase of 195,100 mt compared to the actual production of cold-rolled commercial steel last month, representing a growth of 5.0%.

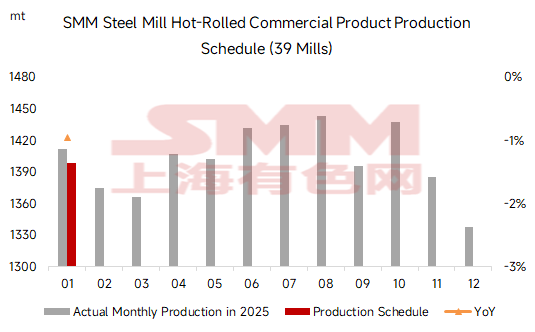

- SMM HRC Production Schedule: January HRC production schedule up 4.6% MoM.

According to the latest SMM tracking, the total planned volume of HRC commercial material from 39 mainstream steel mills this month was 13,988,300 mt, up 613,300 mt MoM from the actual HRC commercial material production last month, an increase of 4.6%.

Entering January, some steel mills that had undergone maintenance earlier gradually resumed production, driving a significant rebound in the production schedule of hot-rolled coils for January. However, in some markets, there is increased pressure on steel mills to take orders for cold-rolled products, or situations where the profits for rebar and medium plates are better than those for hot-rolled coils. This has led some steel mills to make minor adjustments, such as shifting from cold-rolled to hot-rolled production, from coils to rebar, or from coils to medium plates.

Maintenance side, the impact from maintenance on hot-rolled production in January is tentatively 786,200 mt, down 876,600 mt MoM. Currently announced maintenance is concentrated in east China, north China, and central China, with additional reductions in hot-rolled output at some steel mills due to blast furnace maintenance.

Summary: Driven by steel mills resuming production after maintenance, the hot-rolled commercial steel production schedule in January increased by 4.6% MoM from the previous month. Demand side, with the approach of year-end, demand for sheets & plates in January is expected to continue declining compared to December, and inventory may begin to accumulate in the middle and late part of the month, leading to a heightened supply-demand imbalance.

Recently, supported by both fundamentals and market news, furnace charge trends and steel cost support have been relatively strong. However, considering the persistent weakening of actual demand, it is difficult to sustain a continuous rise in hot-rolled coil prices. The price of sheets & plates in January is expected to show strength first and then weaken, with the average price fluctuating within a limited range compared to December.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)